1. UK Property Market Data2. Comparison of Passive Income from Investment Tools3. Pros and Cons of HMOs (Houses in Multiple Occupation)4. Solutions to HMO (House in Multiple Occupation) Disadvantages4. Process of Buying a Second-hand Property in the UK5. Uncovering Major Pitfalls in UK Property Taxes |

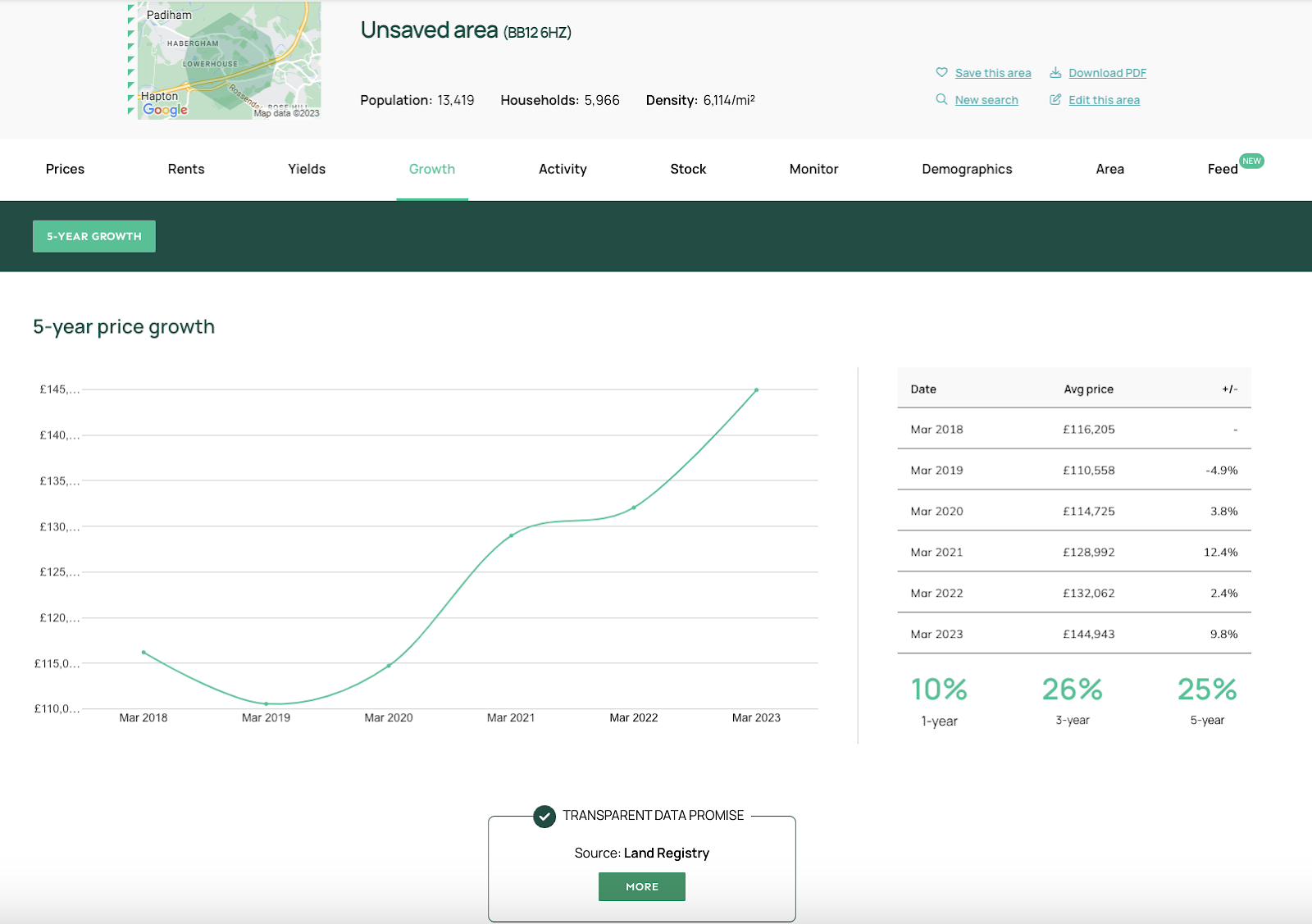

UK property market has tripled over the past 20 years, with short-term rental demand continuing to rise

The high property prices in big cities are something you, living in Hong Kong, would totally understand. This phenomenon makes 'investing in bricks' a reliable investment tool. Looking at the UK, property prices are also standing strong. For instance, in Manchester, the second largest city in the UK, property prices have risen by 315% over the past 20 years.

In terms of demand, from 1996 to 2022, the number of rented households has increased by more than 130%. Despite the surge in demand, there is a severe shortage in the UK housing market, with insufficient supply of new houses. There is a significant imbalance in rental demand and supply in every region of the UK. Capital Economics predicts that rents will continue to rise rapidly in 2023, with an estimated increase of 5.3% by mid-year. With the long-term rise in property prices and the short-term increase in rents, many people are becoming interested in the UK property market.

Moreover, with the hot trend of Hong Kong people moving to the UK, the number of Hong Kong people applying for BNO Visas has exceeded 100,000. Many people are considering buying property in the UK for their own use or for rental, enjoying a peaceful life and earning passive income. However, buying property in a foreign place can be tricky due to unfamiliarity, and it's easy to encounter obstacles. Therefore, we will explain the main process and considerations of buying property in the UK, and uncover the complexities and difficulties.

Comparison of Passive Income from Investment Tools

Speaking of passive income, according to the analysis previously done by the property investment experts at MyHMO, in summary, properties, fixed deposits, and insurance are all low-risk, high-stability investment tools. All three have low liquidity. However, UK HMOs (What is a UK HMO) However, HMOs in the UK outperform the other options in terms of annual return rate, guaranteeing more than 8%. In fact, just like the situation in Hong Kong, subdividing the property into smaller units for rental in the UK will generate a larger rental profit. Moreover, as previously mentioned, the rental return in the UK itself is higher than that in Hong Kong, so naturally, the return rate of UK HMOs is generous.

Pros and Cons of Major Investment Tools: The Devil is in the Details

However, before investing, it's essential to fully consider the pros and cons of the tool. The advantages of UK HMOs are high return rate, low risk, and high stability. However, their disadvantages include more regulatory laws, more troublesome maintenance and repair, tax issues, and more complicated tenant management. The following table provides a deeper look:

| Pros | Cons |

| Long-term investments with relatively low risk, most properties will appreciate over time | Many mortgage lenders carry out stress tests; rental income has to be 145% higher than the mortgage payment under the stress test interest rate (e.g., 5.5%). |

| You can also make a profit in the short term, as long as the rent collected can cover the mortgage loan. | Need to consider regulations (you can choose to have a rental agency handle this) |

| In 2023, the demand for rental housing far exceeds the supply of rental properties, which means you can find tenants. | Need to consider stamp duty, insurance, and operating costs. |

| If the tenant does not pay rent regularly, the property owner still has to bear the monthly mortgage. |

How can MyHMO help you?

In fact, the establishment of MyHMO aims to solve the pain points that many UK property investors are facing. With 18 years of property investment experience, we believe in the potential of UK HMOs. Precisely for this reason, we want to identify the common pitfalls of investing in UK HMOs and find ways to solve them for prospective property owners.

| Cons | MyHMO Solution |

| Many mortgage lenders carry out stress tests; rental income has to be 145% higher than the mortgage payment under the stress test interest rate (e.g., 5.5%). | All second-hand properties of MyHMO have an annual rental return of over 8%. |

| Need to consider regulations (you can choose to have a rental agency handle this) | Renting out HMO requires the property owner to hold an 'HMO license' and the property must fully comply with regulations. MyHMO property experts will closely follow the process of buying a property and collecting rent to ensure nothing goes wrong. |

| Need to consider stamp duty, insurance, and operating costs. | MyHMO property experts will calculate the tax cap for prospective property owners before buying a property to ensure that property owners understand all charges before purchasing. |

| If the tenant does not pay rent regularly, the property owner still has to bear the monthly mortgage. | MyHMO properties are contracted by the UK government. The government and its real estate merchants will recruit tenants and manage rentals on behalf of the property owners. |

-

Process of buying a second-hand property in the UK

The process of buying and selling second-hand properties is open and clear. From one-on-one consultation to signing the lease and finding the tenant, it only takes 4 months. Moreover, MyHMO will go a step further by having a one-on-one consultation with the buyer before introducing the property to understand the client's needs, and after the renovation, we will help invite relevant government officials to inspect the property to ensure that everything is completed according to specifications.

| Step | Details | Time required | |

| 1 | One-on-one consultation | Understand your goals, discuss suitable projects and provide recommendations. If needed, referral services for tax accounting, company formation, and mortgages will be provided. | ~7-14 Days |

| 2 | Project Screening | Provide HMOs that can achieve target returns for buyers to reference and select the most satisfactory project. | ~7-10 Days |

| 3 | Complete | Arrange for a lawyer to handle the property transfer process and AML (Anti-Money Laundering) Check. | ~28 Days |

| 4 | Becoming a property owner | After the owner receives the property, we will immediately arrange for renovation works. | ~3 Days |

| 5 | Carry out renovation works | Our project manager will be responsible for supervising the work to ensure that the specifications of the HMO property meet the standards of the city government and housing agency. | ~60 Days |

| 6 | Arrange for a housing agency inspection | During the construction process, and when the work is nearing completion, we will arrange for relevant government officials to inspect the property to ensure that everything is completed according to their specifications. | ~7 Days |

| 7 | Signing the lease | After passing the inspection, the agency will arrange a lease and sign it directly with the owner. After signing, the rent will be automatically transferred to the owner's UK bank account every month starting from the next month. | |

2. UKProperty Taxes

In addition to the down payment, legal fees, and mortgage broker fees when investing in UK properties, related UK property taxes also arise. Whether in the process of buying and selling or renting, different taxes are involved. If you intend to become a UK property owner, you need to pay attention to these.

Firstly, whether you are a UK citizen or an overseas buyer, simply put, when buying and renting out a property in the UK, you need to pay attention to the following three types of taxes:

- Stamp Duty Land Tax

- Income Tax

- Capital Gains Tax

UK Citizens VS Non-UK Citizens

Among them, the UK Stamp Duty is the largest. For properties priced above £125,000, the tax rate varies from 2% to 12%. For landlords who buy properties for rental income, they need to pay income tax on the rental income. UK citizens enjoy a tax-free allowance of the first £12,500, while overseas buyers pay 20% to 45% income tax annually on income after deducting expenses such as ground rent, property management fees, and council tax.

Additional Stamp Duty Land Tax for Overseas Buyers*

Stamp Duty is required to be paid by the buyer within 14 days after the transaction. Each property only requires payment of Stamp Duty once. The Stamp Duty rate is based on the property price and the buyer's own property situation.

For non-UK residents, if the UK government determines that the purchased property will not be used as the main residence, you can refer to the following:

| Property Purchase Price | Tax Rate |

| £250,000 | 5% |

| £250,001 – £925,000 | 10% |

| £925,001 – £1.5M | 15% |

| £1.5M Above | 17% |

*Starting from April 1, 2021, the UK government has imposed an additional 2% 'UK Overseas Property Tax' on all non-UK nationals and overseas property buyers. Therefore, for those planning to buy property in the UK, in addition to the general expenses of buying a property, they need to reserve 'ammunition' for tax expenses.

For more details, you can visitUK Government Official Website – Stamp Duty Land Tax

Income Tax

If a property in the UK is used for rental, the rental income received is considered taxable income, so personal income tax needs to be paid. Taxpayers need to declare on the UK government website during the tax year.

The tax rate is determined according to the income tax region. In England, Wales, and Northern Ireland, the rates are 20%, 40%, or 45%; in Scotland, the rates are 19%, 20%, 21%, 41%, or 46%.

Some of the expenses used for the property can be used to offset tax costs, such as rental agency fees, property maintenance fees, and council taxes. When declaring, remember to pay attention to the declaration items to reduce the tax.

Capital Gains Tax

When selling a property used for investment rental and making a profit, any gains need to be reported to HMRCthe relevant authorities, and the Capital Gains Tax must be paid within 30 days after selling the property.

The Capital Gains Tax rate depends on the limit of Income Tax. After deducting stamp duty, attorney and real estate agent fees, if the actual gain is £12,571 – £50,270 (Basic Rate), you need to pay 10% of the gain (or 18% for property) as Capital Gains Tax; if the actual gain is £50,271 – £150,000 (Higher rate), you need to pay 20% of the gain (or 28% for property).

For more details, you can visitUK Government Official Website – Capital Gains Tax

3. Unveiling the Traps

Above we have mentioned some potential risks such as (1) numerous taxes, (2) need to consider regulations, (3) if the tenant does not pay rent regularly, the owner still has to bear the monthly mortgage, etc. Below, we will mention three more to make it safer for investors.

-

Is the prime location definitely the best area?

When buying property, people in Hong Kong tend to buy in prime locations near the city center, hoping for high appreciation potential. However, sometimes they overlook the following points:

- The price in prime locations has already risen significantly, and there is limited room for further increases in the future.

- The types of properties in prime locations may not be suitable for investment, for example, many investors favor 'terraced houses', but many core locations no longer have them, instead there are many newly built high-rise buildings.

- The prices of properties in prime locations are relatively high, probably between £400,000 and £500,000, which exceeds the average price of properties in the UK (about £190,000 to £230,000), reducing customers' willingness to buy. They will tend to look for properties close to the average price, and the peripheral areas of prime locations may therefore become popular.

-

Pay attention to the school network, security, and geography near the property area for more stability

If the HMO (House in Multiple Occupation) you buy is in a student area, but the university within the student area is building new dormitories and requires first-year students to live in the dormitories provided by the school, it will reduce the number of people looking for HMOs in the market, and the risk of investment will be relatively higher.

I suggest that you can choose some more stable types of properties, such as investing in second-hand, freehold terraced houses. These are more suitable for some family customers and can also be converted into HMOs (Houses in Multiple Occupation); these types of houses are in high demand in the market and the return on rent will also be higher. In terms of location, the surrounding areas of large cities are suitable, such as London, Birmingham, and Manchester. Many terraced houses in the vicinity are very popular. Many people working in the city center, if they want to live cheaper, will choose to live in these peripheral terraced houses.

-

Calculate clearly the miscellaneous expenses outside of the property price and taxes to avoid losing money

Besides the property price, prospective homeowners must pay attention to different types of expenditures before buying a property. Below are the initial expenses (excluding property price and taxes) mentioned by MyHMO experts. Homeowners should consider the following expenses to avoid finding out 'there are so many extra charges' when buying a property later.

- Legal fees: Prospective buyers need to reserve funds to pay legal fees, generally speaking, about £400-£1500, depending on the region and the complexity of the property. This may also include costs for accelerating the completion of the case, and fees for the lawyer to conduct land registry searches or verify planning documents.

- Brokerage commission: If the transaction involves a second-hand property, a brokerage commission needs to be paid, but it is usually borne solely by the seller. It is generally 0.75%-3.5% of the property price, plus VAT.

- Bank application fee: As mentioned above, if the property purchase involves a mortgage, the bank will charge an 'arrangement fee' and a 'reservation fee' as costs for reviewing documents, different banks charge differently. During the application period, borrowers are also required to conduct a basic property valuation, which is around £150 to £700. In addition, some banks require buyers to submit a 'Homebuyer’s Report' and a building survey, with fees ranging from £350 to £500.

In conclusion: Taxes, hidden charges, and long-term administrative costs are the biggest risks

With the long-term optimistic view of property prices in the UK and the increasing number of people from Hong Kong immigrating to the UK, HMOs as an investment tool have advantages in terms of low risk, high stability, and high annual return rate. But in the situation of 'buying a cow from a distant mountain' and because there are many regulations to comply with, buyers should consult with trustworthy professionals in detail before purchasing. Make sure you understand the taxes, miscellaneous fees, and procedures to be more confident before making any decisions.